Insight: FEOC Compliance in 2026: The Key Challenges for Developers

The consequences of FEOC non-compliance are real; Emily Kuhn-Keaveny, a CoralPoint Partner based in our New York office breaks down some of the key risks for developers and investors and our own approach to due diligence.

Foreign Entity of Concern (FEOC) rules, significantly expanded under the One Big Beautiful Bill Act (OBBBA), restrict clean energy developers and investors from claiming key federal tax credits if their projects involve ownership, control, or material supply-chain assistance from entities tied to China, Russia, North Korea, or Iran (or, known as “PFEs” – prohibited foreign entities), creating substantial compliance, financial, and timing risks across the entire project lifecycle.

Although Treasury guidance is still incomplete, procurement and investment decisions cannot wait for full clarity, and the stakes are high.

Non-compliance can mean losing Investment Tax Credit (ITC) or Production Tax Credit (PTC) eligibility, with clawback exposure years after COD. Meaning, if an entity claims a credit and makes effective control payments to a PFE, the IRS can claw back 100% of the credit.

Here’s a breakdown of some of the key risks.

1. The MACR Calculation Is New and High-Stakes

IRS Notice 2026-15 (issued February 2026) transforms FEOC compliance from a policy concept into a quantifiable financial test. The Material Assistance Cost Ratio (MACR) now directly determines tax credit eligibility.

The MACR will apply to projects beginning construction in 2026 or later. BESS developers will be most affected by the MACR calculations, as battery cells often account for 40–60% of the cost table, and most cells currently come from covered foreign nations.

The Good News for Wind Developers

For a typical US onshore wind project, the major cost components are predominantly sourced from the US, Europe, or India. At a 40% non-Prohibited Foreign Entity (PFE) threshold, most of these projects are very likely to pass. However, wind developers will want to start planning ahead for when the thresholds increase in the coming years.

2. Incomplete Regulatory Guidance Creates Planning Risk

Beyond the MACR guidance, the IRS Notice 2026-15 is silent on many other critical aspects of the PFE requirements. For example, there is some discussion of how “effective control” will be determined, but it does not finalize key definitional tests.

Until the definitions of effective control and other definitional questions are resolved, taxpayers will face significant diligence burdens and continued uncertainty.

The IRS has committed to issuing safe harbor tables, by 12/31/26. Until then, taxpayers claiming the ITC or PTC may use the domestic-content safe-harbor tables in the Domestic Content Bonus guidance issued by the IRS.

3. Supplier Identification Is Tedious and Time-Consuming

Developers and equipment buyers need visibility into a supplier’s ownership, debt, and other sensitive information to determine PFE/FEOC status for material assistance calculations.

This process is time-consuming as it requires evaluating ownership, debt, and management to ensure the company is not controlled or influenced by the covered nation.

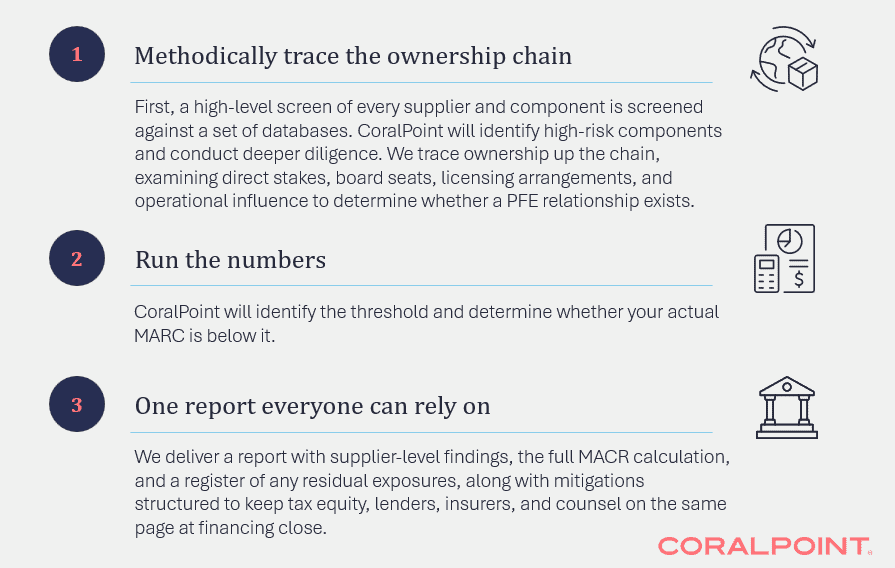

Exhibit 1: CoralPoint’s Approach to Diligence

At CoralPoint, we’ve developed a methodology and report for Material Assistance Compliance that covers the diligence and clearly outlines the approach so developers, tax equity investors, lenders, and counsel can all stand behind it. We work closely with legal teams and tailor our work to each transaction, because this isn’t a one-size-fits-all problem.

For further information, please reach out to: Emily Kuhn-Keaveny