Flash Note: What AR7 Tells Us About the Future of UK Energy

A White Paper on the UK’s largest-ever clean energy auction

Authors: Dr. Lee Clarke (CoralPoint Partner & Senior Advisor), Emilie Reeve (CoralPoint Partner)

The UK’s largest-ever clean energy auction is more than a policy milestone. It reshapes the economics of Britain’s power sector – and the strategic calculations for every organisation that depends on it.

Over the course of just four weeks in early 2026, the UK Government secured more new clean energy capacity than in any previous auction cycle. The results of Allocation Round 7 (AR7) arrived in two stages – offshore wind in January, followed by solar, onshore wind and tidal in February – and together they represent a step change in the scale and credibility of the UK’s energy transition.

The numbers speak clearly. In January, a record 8.4GW of offshore wind was contracted across seven projects, making it the largest offshore wind auction ever held in Europe. Fixed-foundation projects secured a blended strike price of approximately £91/MWh, while two floating offshore wind projects came in at £216/MWh. Then, on 10 February, the second tranche delivered a further 14.7 GW across 201 projects – predominantly solar, onshore wind and tidal – bringing the combined AR7 total to over 23 GW of new clean capacity.

That is an extraordinary volume. But the more interesting story lies in what these results tell us about cost, security and the pace of structural change in the energy system.

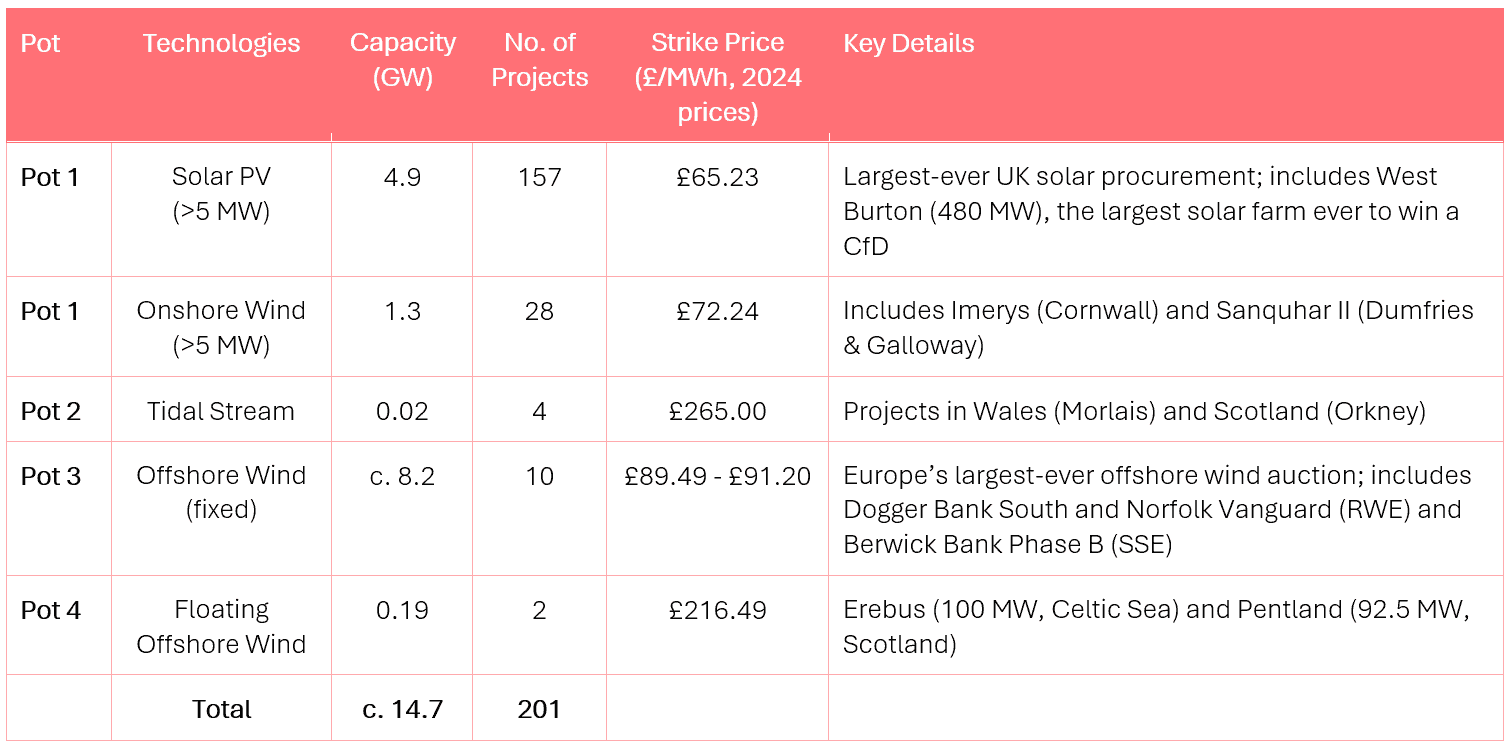

The AR7 auction was split into two stages: AR7 (Pots 3 and 4, offshore wind, announced 14 January 2026) and AR7a (Pots 1 and 2, established and emerging technologies, announced 10 February 2026). The combined results are set out below.

Exhibit 1: AR7 Results Summary by Pot

The Economics Have Moved Beyond Debate

For years, the cost competitiveness of renewables has been a topic of discussion. AR7 should settle that discussion for the UK market.

New onshore wind cleared at £72.24/MWh and solar at £65.23/MWh; both under half the £147/MWh the government estimates it would cost to build and operate a new gas-fired power station. Offshore wind at £91/MWh is similarly well below that benchmark.

These are not theoretical projections. They are contracted prices, underpinned by 20-year CfD agreements that provide revenue certainty for developers and cost visibility for the system.

Some commentators have questioned whether comparing CfD strike prices to new-build gas is fair. Carbon Brief’s recent analysis addresses this directly: the £147/MWh gas figure reflects the government’s latest cost of generation estimates, which account for recent inflationary pressures on turbine supply chains – pressures that have more than doubled the estimated cost of building a gas-fired plant. Comparisons citing much lower gas costs, such as the £55/MWh figure used by some opposition politicians, strip out the cost of carbon pricing, ignore the capital cost of new plant entirely, and fall below even 2025 wholesale prices, which averaged around £80/MWh. The lower figures are unrealistically low because they refer to existing rather than new gas-fired plants, which would need to recover much increased Capex costs.

The Political Backdrop

AR7 lands in the middle of an increasingly polarised political debate over net zero in the UK. The cross-party consensus that held for nearly two decades, from the Climate Change Act 2008 through to the legislating of the 2050 net zero target in 2019, has fractured. The Conservative Party, under Kemi Badenoch’s leadership, has pledged to repeal the Climate Change Act and has characterised the net zero transition as “fiction” that is “making our country less safe, less secure, and less resilient”. Reform UK has gone further, openly challenging the scientific basis for climate action and vowing to “wage war” on renewable energy developers.

At the centre of the opposition argument is the claim that green policies are driving up electricity bills. But that claim sits awkwardly alongside the AR7 evidence. AR7’s results do not resolve the political argument, but they do shift the burden of proof: with clean power now demonstrably cheaper, more secure and domestically generated, the case for retreating from the transition has become considerably harder to make on economic grounds.

Landmark Projects, Real Transformation

Several of the projects awarded through AR7 carry particular weight – both symbolic and economic.

West Burton, the site of the UK’s last coal-fired power station in Nottinghamshire, has secured a CfD as the largest solar farm ever to win a government renewables contract. At up to 480 MW, it could power approximately 144,000 homes. The Imerys Wind Farm in Cornwall becomes the largest onshore wind project successful in England in over a decade, and Sanquhar II in Dumfries and Galloway reinforces Scotland’s wind contribution.

On the offshore side, Dogger Bank South (3GW) and Norfolk Vanguard (3.1 GW) will be among the largest offshore wind farms in the world, while Berwick Bank in Scotland (4.1 GW) is the single largest planned offshore wind project globally. Notably, 83% of the offshore capacity connects in areas of high power demand and greater network capacity, which should help limit system balancing costs.

Collectively, the government estimates the February tranche alone will unlock around £5 billion in private investment and support up to 10,000 jobs. Combined with the offshore round, total private investment across AR7 approaches £27 billion.

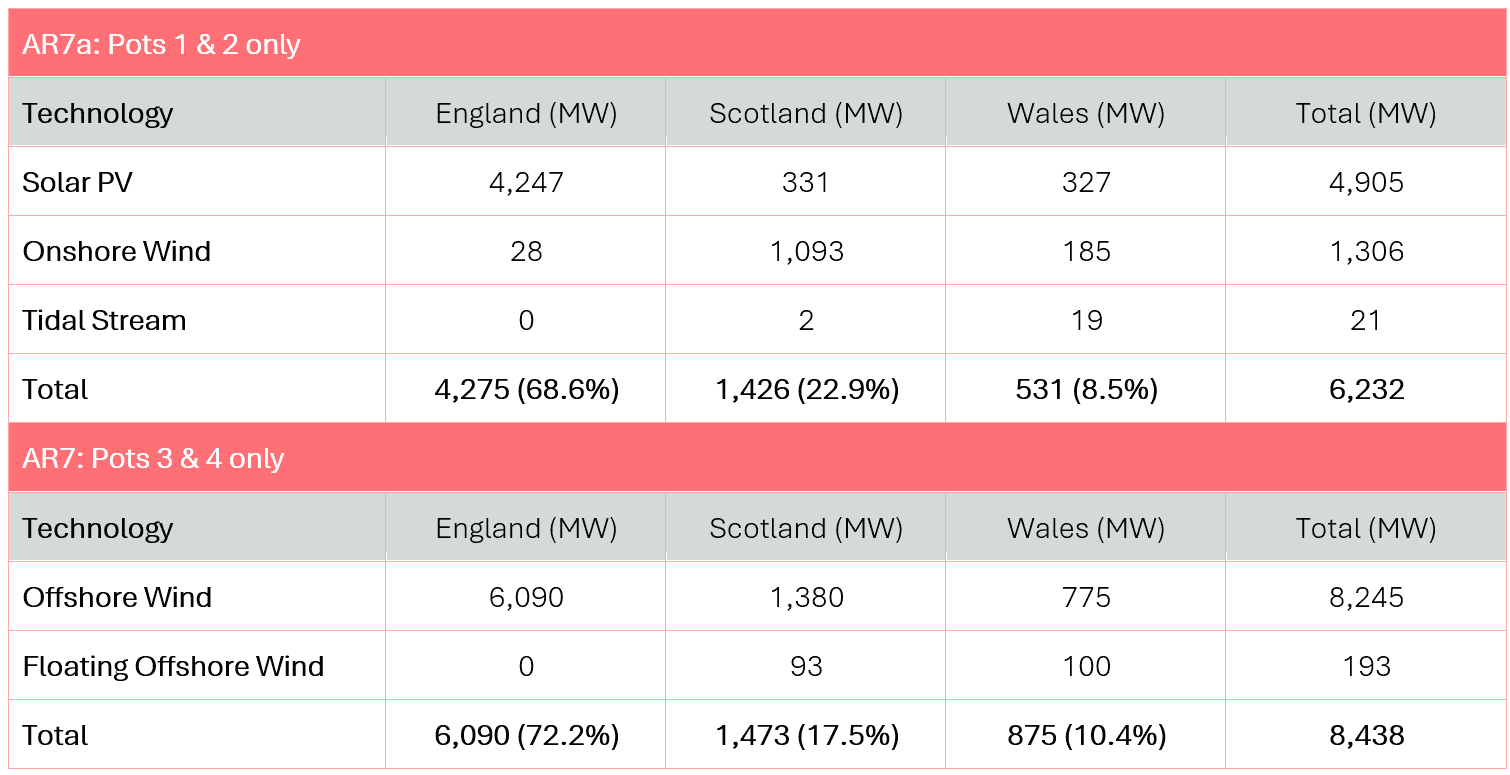

Exhibit 2: AR7 Results Summary by Region

Clean Power by 2030: Within Touching Distance

AR7 has materially narrowed the gap to the UK’s target of decarbonising the power system by 2030. NESO’s independent advice calls for 43-51 GW of offshore wind capacity to meet that goal. With around 17 GW installed today and a further 10 GW already contracted through previous rounds, the 8.4 GW secured in January’s offshore auction leaves a remaining gap of roughly 7 GW to the lower end of that range. Chris Stark, head of Mission Control for Clean Power 2030, described the results as putting the UK “within touching distance” of its offshore wind targets.

Of course, significant delivery risks remain. Grid connection timelines, planning and consenting bottlenecks, and supply chain constraints all have the potential to slow progress. Industry observers have been clear that securing auction contracts is only part of the challenge; the projects must actually be built, the network reinforced, and permitting processes streamlined if capacity is to come online on schedule. Some analysts believe a more realistic target may be clean power by the early 2030s rather than exactly 2030, but even on that adjusted timeline, the pace of transformation would be historically unprecedented.

What This Means for Business

For organisations navigating the energy landscape, AR7 carries several strategic implications worth weighing carefully:

- The grid is being rebuilt around renewables – now! The CfD scheme has contracted over 47 GW of renewable capacity in total. Corporate energy strategies that remain anchored to gas-priced wholesale assumptions are increasingly misaligned with the direction of the system.

- Clean power is the cheapest new power. This is not an aspirational statement; it is what the auction data shows. Businesses still treating low-carbon procurement as a premium are working with outdated assumptions. The convergence of cost and carbon performance changes the calculus for PPAs, on-site generation and energy efficiency investment.

- Location decisions should follow electrons. Regions hosting major AR7 projects – Cornwall, Dumfries and Galloway, Nottinghamshire, East Anglia, Yorkshire – will benefit from infrastructure, jobs and access to lower-cost generation. For energy-intensive sectors, proximity to abundant renewable supply is becoming a genuine strategic factor.

- Flexibility is where the next wave of value sits. As intermittent renewables grow in share, organisations that can shift demand, store energy or provide grid balancing services will be increasingly well positioned. The merit order effect means that periods of high renewable output drive wholesale prices lower, creating opportunities for those who can consume or store energy flexibly.

Looking Ahead

AR7 represents something more substantive than a record-breaking auction. It is evidence that the UK’s clean power ambitions are translating into contracted, investable, cost-competitive capacity and at a scale that is beginning to reshape the structure of the energy system itself.

For policymakers, it validates the CfD mechanism as a delivery tool. For investors, it reinforces the UK as a credible market for long-duration clean energy assets. And for business leaders, it poses a straightforward question: given where the energy system is heading, and how quickly, how should your organisation be positioning itself to benefit?

The direction is clear. The pace is accelerating. And the window for early-mover advantage is narrowing.

Sources

UK DESNZ (Jan 2026). Press release: Record breaking auction for offshore wind secured to take back control of Britain’s energy. https://www.gov.uk/government/news/record-breaking-auction-for-offshore-wind-secured-to-take-back-control-of-britains-energy

UK DESNZ (Feb 2026). Press release: New auction delivers unprecedented clean, homegrown power. https://www.gov.uk/government/news/new-auction-delivers-unprecedented-clean-homegrown-power

UK DESNZ (Feb 2026). Contracts for Difference (CfD) Allocation Round 7: results. https://www.gov.uk/government/publications/contracts-for-difference-cfd-allocation-round-7-results

Carbon Brief (Jan 2026). Q&A: What UK’s record auction for offshore wind means for bills and clean power by 2030. https://www.carbonbrief.org/qa-what-uks-record-auction-for-offshore-wind-means-for-bills-and-clean-power-by-2030/

NESO (Jul 2025). CFD Allocation Round 7 and 7A: Contract Allocation Process Guidance Guidance Document Version 1.1. https://www.neso.energy/document/365771/download

Related Articles

Insight: Deep Geothermal Power Generation in the United Kingdom

Hamburg Declaration: A Clean Energy Security Pact Reshaping the North Sea

FLASH NOTE: U.S. House of Representative’s Permitting Reform Bill: How the SPEED Act Helps–and Hurts–Project Certainty

Denmark’s Offshore Wind Market: Lessons, Reforms and New Momentum