Insight: Tidal Power’s Moment of Reckoning

Britain has the tides, the technology and the expertise. What it lacks is the nerve

Authors: Dr. Lee Clarke (CoralPoint Partner & Senior Advisor)

Britain is unusually well placed for tidal energy. With roughly 50% of Europe’s tidal resource around its coasts, it has a natural advantage in a technology that promises something almost no other renewable can deliver: electricity generated to a timetable, predictable years in advance, regardless of whether the wind blows or the sun shines. The National Energy System Operator’s (NESO) Future Energy Scenarios anticipate between 1.7 GW and 4.3 GW of tidal capacity by 2050 as part of credible net-zero pathways. It is an industry that has been on the cusp of commercial viability for the better part of a decade.

It remains there still

The Wreckage from a Single Month

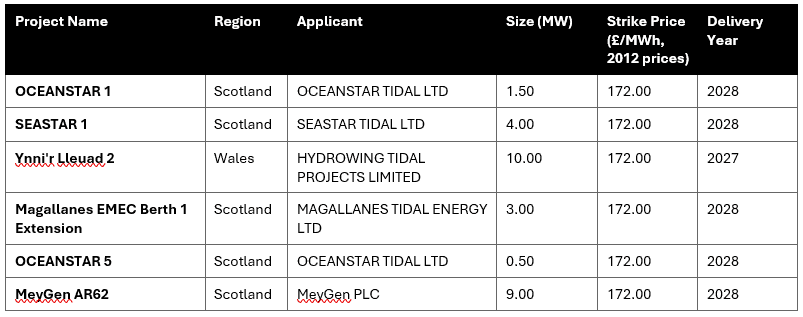

The evidence is not theoretical. In the second week of May 2026, the Low Carbon Contracts Company quietly published termination notices for three tidal stream projects that had won 15-year government subsidy contracts less than two years ago. Seastar 1, Oceanstar 1 and Oceanstar 5 (all developed by Edinburgh-based Nova Innovatio) had their Contracts for Difference (CfDs) scrapped simultaneously. Combined, they represented 6 MW of capacity at the European Marine Energy Centre’s Fall of Warness test site in Orkney, contracted at a strike price of £172/MWh – a figure that, adjusted for inflation since award, had already climbed to £253.90/MWh.

The three cancellations accounted for half of the six tidal stream contracts the government had awarded in its sixth CfD Allocation Round (AR6) in September 2024. The economics that underpinned bids at the time of auction had, by the time of financial close, been eroded by cost inflation and a persistently difficult financing environment.

Contracts for Difference (CfD) Allocation Round 6: results

Scale First, Savings Later

To understand why tidal stream keeps stumbling, its position on the cost curve matters enormously. The ORE Catapult estimates the levelised cost of energy for tidal stream at approximately £259/MWh – already a reduction of more than 40% from an estimated £300/MWh in 2018, achieved with minimal commercial revenue support. The ORE Catapult’s modelling suggests costs could fall to £78/MWh by 2035 and to below £50/MWh thereafter, but only if deployment reaches the scale needed to realise volume and learning-curve efficiencies.

Therein lies the central difficulty. Costs fall through deployment. Deployment requires financing. Financing requires costs to already be competitive. It is precisely the dilemma that confronted offshore wind in the early 2010s – but a technology the government chose to support with sustained subsidy until the economics improved. Offshore wind’s CfD strike price fell from around £155/MWh in the first auction round to below £45/MWh a decade later. That trajectory was a policy choice, not an accident.

The UK has only around 10 MW of tidal stream capacity installed and operational today – representing more than half of the world’s total. Nova Innovation’s SEASTAR project, had it proceeded, would have deployed 16 turbines in a single array – the largest ever attempted. The cancellation is not merely a setback for one company; it removes what would have been the most significant demonstration of array-scale cost reduction in the sector’s history.

Too Little, Too Late

The CfD ringfence for tidal stream – the dedicated slice of auction budget that prevents the technology from having to compete directly against mature, far-cheaper solar and wind – is the policy mechanism on which the sector depends. Without it, no tidal project would clear the auction threshold.

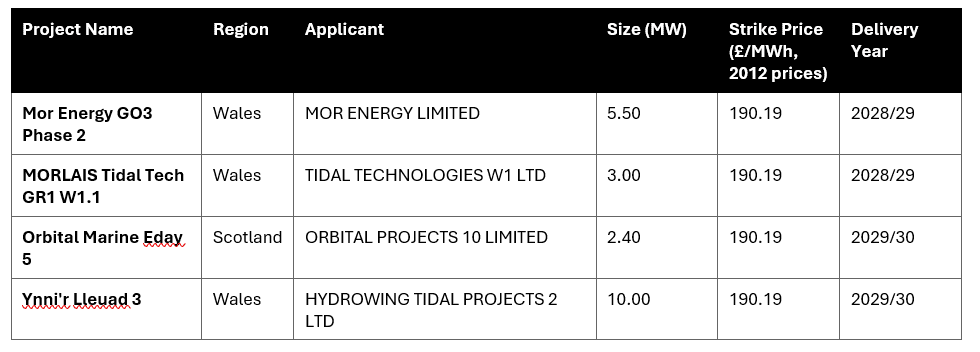

The Marine Energy Council lobbied for that ringfence to be set at £30 million in AR6. The government awarded £10 million – enough, on the published forecasts, to secure roughly 13 MW of additional capacity. In the subsequent AR7a auction, completed in February 2026, the Pot 2 budget, which was shared across six competing emerging technologies, was cut to £15 million, with no technology-specific ringfence. Four tidal projects won contracts, totalling 20.9 MW at a clearing price of £190.19/MWh in 2012 prices, but only by displacing other emerging technologies from the same constrained envelope.

The structural problem is one of timing. By the time a tidal project moves from CfD award to financial close (typically 12 to 18 months) the macroeconomic backdrop has often shifted materially. Contract prices are fixed at auction; input costs are not. The government’s own CfD reform consultation acknowledged this tension explicitly, noting the need to better align award conditions with the realities of project development timelines. For tidal stream, where developers are smaller and margins thinner, the consequence of each cancelled project is more severe for the sector’s overall cost-reduction trajectory.

Contracts for Difference (CfD) Allocation Round 7a: results

What Remains Standing

Three AR6 tidal contracts remain intact. SAE Renewables’ MeyGen project in the Pentland Firth, which is the world’s largest operational tidal stream facility, with 6 MW already generating, retains its 9 MW AR6 extension contract. HydroWing’s 10 MW Ynni’r Lleuad 2 project off Anglesey, at the Morlais site, Europe’s largest consented tidal energy development, is advancing toward construction. Magallanes Tidal Energy’s 3 MW EMEC extension also remains live.

MeyGen’s operational record matters beyond its megawatt count. Individual turbines have run for more than six years without unplanned maintenance. This is the kind of long-run reliability data that lenders require before committing capital to larger arrays. It is the sector’s most credible proof point, and it underpins the investment case for what comes next.

Enter the Taskforce

The UK government launched a Marine Energy Taskforce in June 2025, commissioned by the Department for Energy Security and Net Zero to develop a strategic roadmap for tidal and wave energy. Led by Energy Minister Michael Shanks and co-funded by The Crown Estate and Crown Estate Scotland, it has engaged over 100 stakeholders across industry, finance and government. Its findings are due in June 2026.

The Taskforce is examining the four pressure points the sector consistently identifies: site development, financing structures, innovation support, and supply-chain capacity. The urgency is clear from the numbers. The University of Edinburgh’s policy modelling, published with Supergen ORE Hub in 2025, suggests that deploying 6.2 GW of tidal stream by 2050 could contribute over £50 billion in gross value added to the UK economy and sustain over 80,000 jobs. NESO’s own analysis suggests tidal generation could reduce wholesale energy prices by around £120 million a year between 2037 and 2060 by displacing peaking generation.

What the Taskforce has not yet resolved is the financing architecture that bridges a CfD award, with the promise of future revenue, and a bank-funded construction contract. That gap claimed Nova Innovation’s three projects. The ORE Catapult’s analysis indicates that costs fall significantly only once the UK reaches approximately 1 GW of cumulative deployment; at current rates of build, that milestone is decades away. The harder question is not whether the UK should pursue tidal energy, but who bears the development risk until costs reach the level where private capital will follow unaided.

The Offshore Wind Precedent

Britain’s situation invites comparison with its own recent energy history. The decision in the early 2010s to commit sustained CfD support to offshore wind, at prices then widely considered excessive at the time, is now regarded as a policy success. The ORE Catapult notes that the cost reduction tidal stream has already achieved since 2018 – more than 40% with minimal subsidy – tracks closely with early-stage offshore wind learning rates. A 2024 paper in Renewable and Sustainable Energy Reviews concluded that at 1 GW of deployment, tidal energy’s cost trajectory becomes firmly competitive. The technology also generates from domestic resources, with over 80% UK supply-chain content at commercial scale, which is a material consideration in an era of energy security anxiety.

The political will for a comparable commitment remains, however, conspicuously limited. The AR6 ringfence of £10 million is a fraction of what the government spent supporting offshore wind at an equivalent stage. The Marine Energy Council’s repeated request for £30 million has never been met. The DESNZ’s own levelised cost analysis of tidal stream, published in 2023, projects a clear cost-reduction pathway, but one that is contingent on deployment volumes that current policy budgets make difficult to achieve.

Next Steps

The May 2026 contract terminations are a setback, but not a terminal one for the sector. The projects that remain – MeyGen, HydroWing, Magallanes – are at the more commercially advanced end of the pipeline. The Marine Energy Taskforce’s roadmap, due imminently, represents the most direct government engagement with the sector’s structural barriers to date.

But the pattern has become familiar enough to be dispiriting: contracts awarded, costs rise, projects fold. Each cancellation delays the cost reductions that would make the next round of projects easier to finance. The UK’s tidal resource is not diminishing. The question is whether the policy framework will move quickly enough to make use of it.

Sources:

NESO Future Energy Scenarios 2025 https://www.neso.energy/document/364541/download

Levelised Cost of Electricity from Tidal Stream Energy (DESNZ, 2023) https://assets.publishing.service.gov.uk/media/655372484ac0e1001277d819/tidal-lcoe-report.pdf

Contracts for Difference Allocation Round 6 Results (DESNZ, September 2024) https://www.gov.uk/government/publications/contracts-for-difference-cfd-allocation-round-6-results/contracts-for-difference-cfd-allocation-round-6-results

Low Carbon Contracts Company CfD Register https://register.lowcarboncontracts.uk

ORE Catapult Tidal Stream Cost Reduction Pathway Report (2022) https://ore.catapult.org.uk/wp-content/uploads/2022/10/Tidal-stream-cost-reduction-report-T3.4.1-v1.0-for-ICOE.pdf

Assessing the Costs of Commercialising Tidal Energy in the UK (Nobel and others, Renewable and Sustainable Energy Reviews, 2024) https://tethys-engineering.pnnl.gov/sites/default/files/publications/Nobel_et_al_2024.pdf

A Review of the UK and British Channel Islands Practical Tidal Stream Energy Resource (Proceedings of the Royal Society A, 2021) https://royalsocietypublishing.org/doi/10.1098/rspa.2021.0469

Marine Energy Taskforce — government proceedings (DESNZ/Crown Estate, 2025–26) https://www.marineenergycouncil.co.uk/news/marine-energy-taskforce-enters-second-phase-following-cardiff-update

What is the value of innovative offshore renewable energy deployment to the UK economy? (Supergen ORE Hub, April 2025) https://www.policyandinnovationedinburgh.org/uploads/3/1/4/1/31417803/supergen_-_value_of_innovative_ore_-_april_2025.pdf

Various company announcements from Nova Innovation, Hydrowing, MeyGen and Elgin Energy